The Volatility of Inflation Expectations and Interest Rates

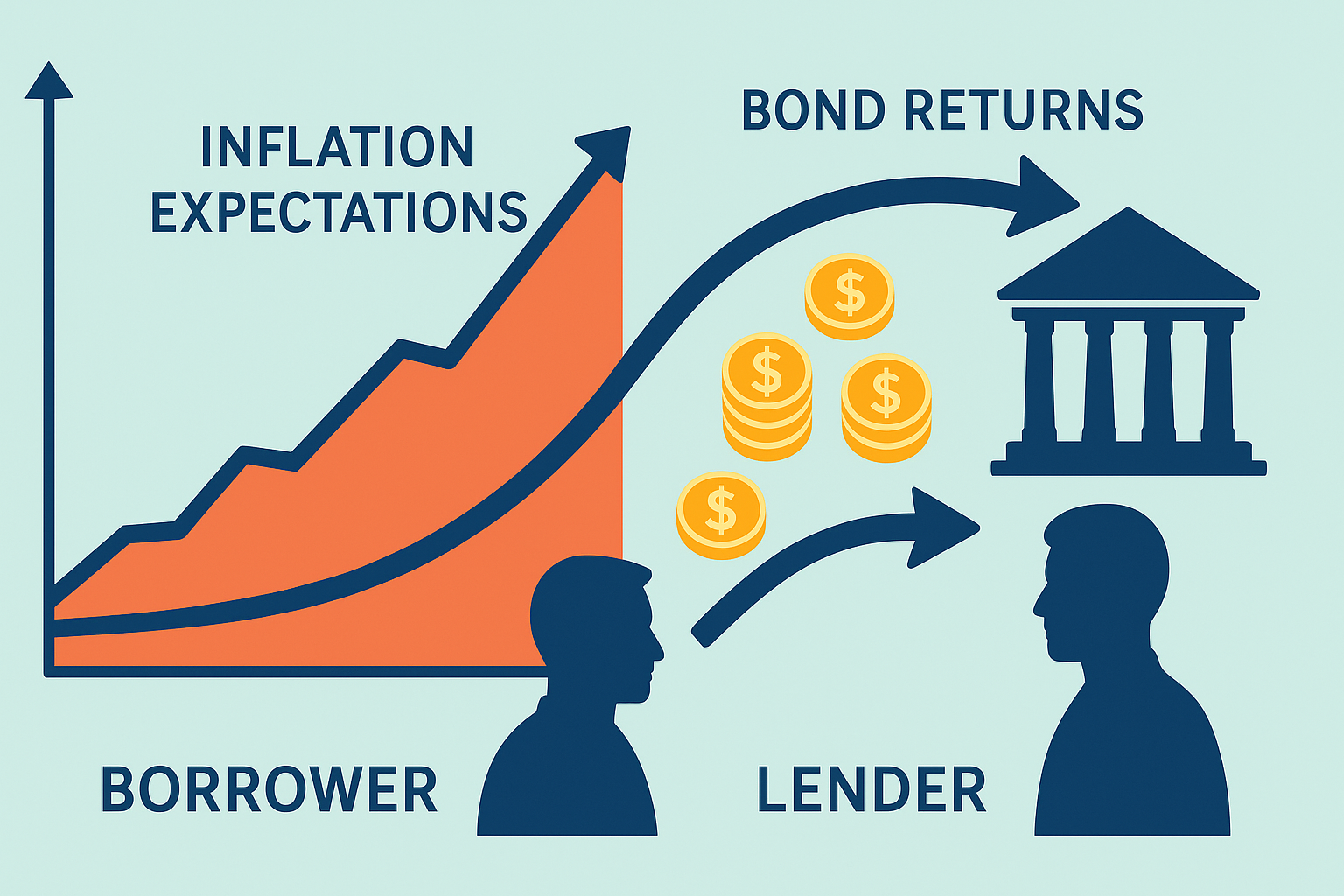

This paper exploits bank forecasts (1989–2022) for 18 advanced economies to show that horizon overreaction to high inflation expectations boosts bond returns, shifting wealth to lenders; a salience learning model explains this bias variation.